In diesem Dossier:

- Metal mining worldwide – and metal deposits in Europe

- Demand for selected metals by future technologies

- There would be no resource scarcity ...

- Mining and gender

- Mining harms the environment and human health

- The EU’s resources policy – part of the «Green Deal»

- The geopolitical importance of raw materials

- Metal extraction leads to unrest and protests: mining-related conflicts in Latin America

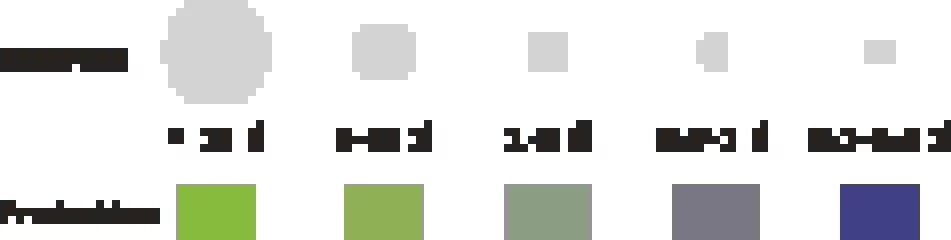

Metal mining worldwide – and metal deposits in Europe

The dots in the graphic below illustrate the calculated value of metal reserves worldwide. The term «reserves» designates deposits that can actually be extracted profitably – rather than those whose availability is purely theoretical. A change in technological or economic conditions can thus lead to a change in reserve volumes. An increase in commodity prices, for example, may make the extraction of metals in remote locations worthwhile that would not make economic sense at lower prices; and new technology may allow access to metals that previously were out of reach. The coloring shows the share of countries in the annual production of metals.

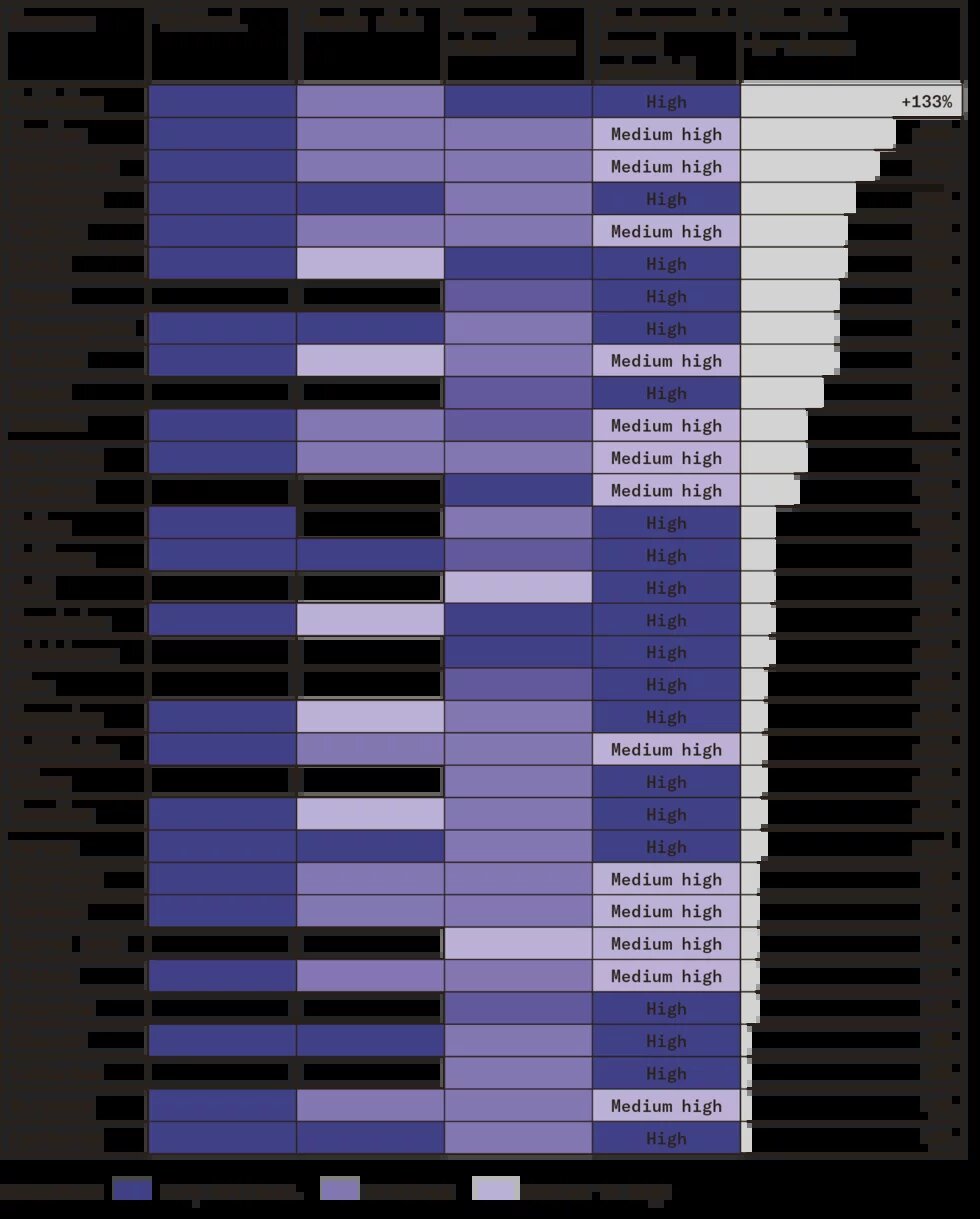

Demand for selected metals by future technologies

The chart shows the potential demand for certain raw materials created by what is often referred to as «future technologies» – e.g. microchips, high-performance lithium-ion batteries, fuel cells, wind turbines or thin-film solar cells. The demand for raw materials can vary depending on which technical innovations, political stipulations and consumption patterns prevail. For example, if equipment is repaired and remains in service longer, the demand for raw materials will decrease. The figures presented are not forecasts, but rather illustrate possible developments that appear realistic based on today’s knowledge.

: DERA Rohstoffinformationen. Rohstoffe für Zukunftstechnologien. Berlin, 2021")

Digitalization, construction and transportation are key drivers

Public discourse suggests that the energy transition is the reason for the strong demand for natural resources. That is not the case. In Germany, for example, the main demand drivers are digitalization, construction and the transportation sector. If sales figures remained unchanged, the batteries for electric Volkswagens alone would require about eight times as much aluminum and nickel in 2030 as the total increase in wind power plants planned for Germany until then. In fact, the production of renewable energies does not actually require significantly larger volumes of metal than the use of fossil energies. Quite the opposite: some renewable energy technologies, such as small hydroelectric plants or roof-mounted photovoltaic systems, have a much smaller «metal footprint» than fossil-fueled power plants, for instance. Put into numbers, a small hydroelectric plant requires 340g of metals to produce one megawatt hour of electricity; a coal-fired power plant needs up to 3,920g, i.e. about ten to eleven times as much.

One thing is clear: The expansion of renewable energy technologies requires large amounts of metals. Their material intensity is still significantly lower than that of conventional power plants, however, since the fossil fuels burned in gas- and coal-fired plants also forms part of the equation.

From the Connecting the Raw Materials Transition and the Energy Transition study by PowerShift with data from the Luxembourg Institute of Science and Technology (LIST).

There would be no resource scarcity ...

... if production and consumption were designed in accordance with a sustainable circular economy. Living spaces would become smaller, electrical appliances would be repaired and eventually recycled, the number of cars would decrease and the few cars remaining would be smaller and lighter. And so on.

This potential for change means: In a sustainable circular economy, large parts of the expected resource demand – for example 61 percent of cobalt and 68 percent of neodymium – could be met by technological innovations, recycling and behavioral changes. Zero percent means: Circular economy measures prevent shortages.

Mining and gender

-

Earnings of women in the extractive sector: a quarter of what men earn

-

In mining countries, women often do not have access to mining rights and titles.

-

Share of women in artisanal mining: between 30 and 50 percent (depending on country and company)

-

Share of women in industrial mining: approx. 10 percent

Mining adversely impacts women:

-

through contaminated soil and water, because it often mainly women who farm and raise livestock

-

through sexual assault as male workers migrate to mining regions

-

because in many countries, they hold no titles to their land. They lose their livelihoods and are not compensated when land is used for mining.

Mining harms the environment and human health

Air pollution: In opencast mining, the wind carries exposed elements such as lead, arsenic or cadmium into the environment. The associated vehicle traffic emits nitrogen oxides and particulate matter. These pollutants can harm the health of people living near the mining site, causing respiratory diseases and allergies.

Water pollution: Acid mine drainage, metals and other contaminants end up in rivers. Pollutants from treatment plants, tailings ponds, underground mines, waste disposal facilities and active or abandoned surface or haul roads are the main sources of water pollution.

Water consumption: The German Federal Statistical Office lists industry and mining as the largest water consumers in Germany. Mining requires water to extract and process the ores. According to a Swedish study, about 92.7 liters of water are needed to extract 1 kilogram of copper. To be fair: Mining and industry in Germany have been using less water lately, while agricultural water consumption is increasing.

Destruction of the landscape: Open pits and spoil tips can impact the landscape and physically destroy the soil, harming local plants and animals. Many of the surface features destroyed by the mining operations cannot be restored once they cease. Removal of soil layers and deep underground excavations can destabilize the ground. Even after renaturation, the land does not regain its original agricultural productivity.

Loss of biodiversity: Pollution and landscape destruction can have catastrophic effects on biodiversity in mining areas. Losses range from soil microorganisms to large mammals. Endemic species, i.e. those that occur only in limited areas or a specific region, are the hardest hit as even the slightest disruption to their habitat can lead to extinction. Toxins released by mining can wipe out entire populations of vulnerable species.

The EU’s resources policy – part of the «Green Deal»

European Green Deal – the overarching strategy

Objective: Climate neutrality of the 27 member states by 2050. Reduction in greenhouse gas emissions by 55 percent from 1990 levels by 2030. Includes numerous individual measures. Learn more.

Critical Raw Materials Act

Objective: Ensuring the supply of critical raw materials to member countries. The list of critical raw materials currently includes 34 items and is continually updated. Sources of raw materials are to be diversified, monitoring and resilience to short-term supply shortages expanded and the circular economy strengthened. The central instrument is the promotion of strategic projects in the context of mining, recycling and processing within Europe and abroad. Civil society criticizes weak environmental and human-rights standards and a lack of targets for a reduction in resource consumption. Learn more.

Corporate Sustainability Due Diligence Directive

Objective: Mitigating or eliminating human rights violations and pollution in the supply chains of European companies in all sectors. It is intended to obligate companies to identify and prevent, end or mitigate adverse impacts of their operations such as child labor, slavery, pollution or loss of biodiversity along their supply chains. Learn more.

Strategic Partnership on Raw Materials

Objective: Securing the supply of raw materials. With its partnerships on raw materials, the EU aims to work with resource-rich countries to create safe, resilient, economical and sustainable supply chains, while promising to promote economic development by creating value chains within the mining countries. Learn more.

Critical Raw Materials Club

Objective: Securing raw material supply chains. Within the framework of a «club for critical raw materials», the EU aims to strengthen global supply chains and the World Trade Organization. The club members want to facilitate investment and expand free trade agreements, and intend to defend themselves against unfair trading practices. This could mean that countries such as Indonesia or Namibia are prevented from developing their own industries for processing raw materials. Many civil society organizations see this as a contradiction to the EU’s declared intent to enable value creation in mining countries in regions such as Latin America and Africa in order to enable them to benefit more from their own natural resources.

Circular Economy Action Plan

Objective: Reducing waste, increasing product sustainability in the EU. Essential pillar of the European Green Deal. Provides for numerous individual measures, such as an eco-design directive to promote re-use and recycling, and a right to repair. Learn more.

The geopolitical importance of raw materials

Interview with Oliver Radtke, Director of the Heinrich Böll Foundation’s Beijing office

Mr. Radtke, what role do raw materials play in China’s foreign policy?China has developed a monopoly on some mineral resources, supplying, for instance, approximately 98 percent of EU imports of rare earths. Beijing uses mineral resources as a trade weapon: Following a 2010 incident near the disputed Senkaku Islands, or Diaoyu Islands, as China refers to them, the Chinese government halted all exports of rare earths to Japan. By the same token, China imposes import stops, for example on coal or lobster from Australia. According to an OECD study, China leads the world in the number of export restrictions on critical raw materials.

How strategic is China when it comes to its own supply of natural resources?

Under the Belt and Road Initiative, Chinese state-owned companies are investing in raw material extraction worldwide, partly to meet China’s own immense and growing demand. China currently consumes 50 percent of global steel production. And it is much better prepared for the coming mineral economy than Europe, as plans for clean technologies – hydrogen batteries, wind and solar power – were developed as far as 15 or 20 years back.

Is China self-sufficient?

No, it is heavily dependent on the import of soft commodities, i.e. lightly processed agricultural products such as soybeans and beef. China imports nearly 80 percent of its annual soy consumption, primarily from Brazil and the United States. This makes it one of the major drivers of (illegal) deforestation in the Amazon and in Mercosur. It now aims to reduce these dependencies. In terms of future industries, China depends on imports of lithium and cobalt, among other things. It will therefore want to establish and expand strategic partnerships with producing countries in Africa and South America.

Interview with Aaron Mintzes, Senior Policy Counsel at Earthworks, Washington, DC

What role does the supply of natural resources play in the Inflation Reduction Act, the US law aimed at combating inflation through investments?The Inflation Reduction Act includes tax credits for the domestic mining and refining of raw materials, as well as for electric vehicles that contain raw materials (metals, batteries and their components) sourced domestically or from countries that have free trade agreements with the US. This is intended to increase the supply of primary and recycled materials. By means of the Inflation Reduction Act and the Investment in Infrastructure and Jobs Act, the government is trying to balance supply and demand for natural resources.

Is the current administration pursuing strategic geopolitics to secure raw material supplies?

Yes. The State Department maintains the Mineral Security Partnership, a global initiative of industrialized countries such as Australia, Canada, France, Germany and others with the aim of ensuring secure and sustainable supplies of raw materials. There is also the Energy Resources Governance Initiative, which focuses on Latin America and is mainly concerned with lithium.

How does domestic mining affect the US population?

In the US, the vast majority of copper, cobalt, lithium and nickel deposits are located within 35 miles of Native American reservations. The legislation that still governs most mining in the US dates back to 1872, i.e. the time of the westward expansion. While the law does require the tribes to be consulted before mining permits are issued, in practice this too often means that the government simply sends a letter or has a representative attend a meeting. No provisions have been made for license fees, for example. Unless there is a legislative reform, the mineral rush of the 21st century will only repeat the mistakes of the past.

Metal extraction leads to unrest and protests: mining-related conflicts in Latin America

- Known conflicts: 284

- Cross-border conflicts: 5

- Mining projects involved: 301

- Cases of criminalization of protests: 264

- Mining-related referendums: 39

- Water conflicts: 162