1. What does “sovereign debt” mean? Why is this topic important?

Governments borrow money to manage their finances and invest in projects – these debts are known as sovereign or public debts. When a government takes on more public debt than it can service, there are serious consequences. Crippling principal and interest payments and penalties force cuts in public budgets and vital services, which sacrifice human well-being and long-term growth prospects. In our globalized world, one country’s over-indebtedness can have spillover effects on regional or even global markets, as we saw in the recent Greek financial crisis.

We currently lack an effective insolvency regime that could resolve sovereign debt crises in a fair, speedy and sustainable manner. Due to this governance gap, governments are forced to tackle debt overhangs with austerity policies. As officials of the International Monetary Fund (IMF) state, austerity, or the contraction of government spending inevitably fosters inequality and unemployment, while creating a drag on long-term growth.[1]Growth is central to the G20 mission. (See #4 on Growth of this series.) Moreover, the risk of a global debt crisis poses a serious threat to the achievement of the recently adopted UN Sustainable Development Goals (SDGs), which all countries in the world pledged to achieve by 2030.

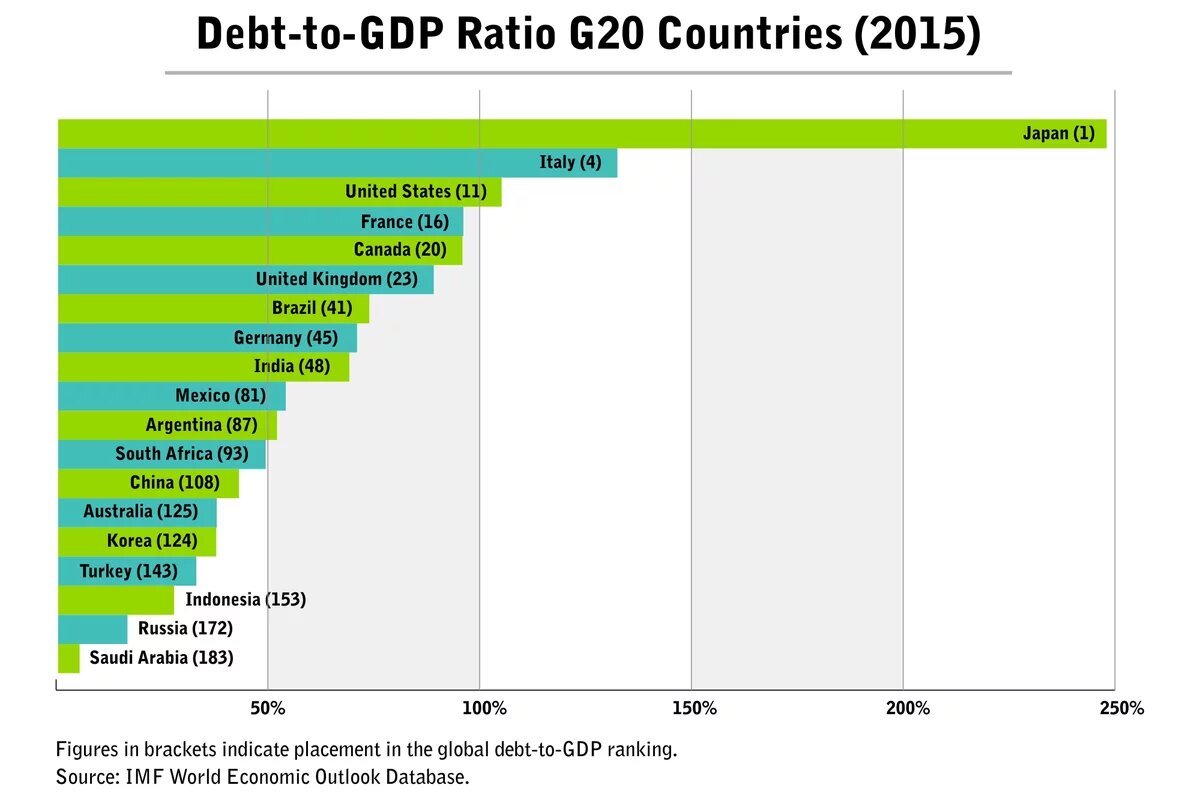

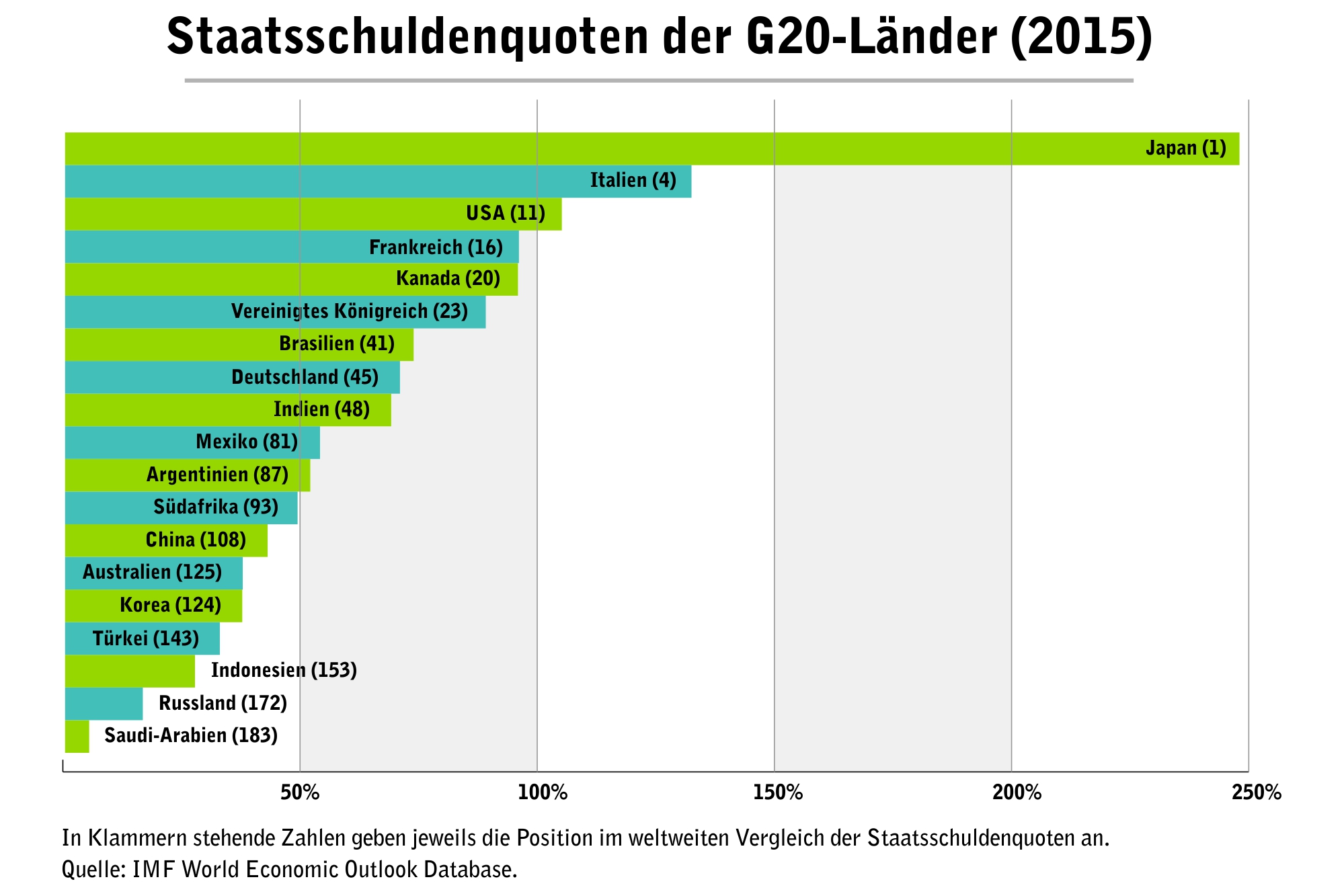

As consequence of the financial crisis, the wealthy G20 governments have contracted a staggering amount of debt. Of the $60 trillion outstanding world public debt, the US share is just under 30 per cent, followed by Japan at just under 20 per cent. To put this in context, world public debt is 82 per cent of the gross world product (GDP) of about $73 trillion.

Some G20 countries are among those with an alarmingly high debt to GDP ratio (see graph below). Of the top 20 countries with the highest such ratio, four are G20 member countries, with Japan leading the pack - its sovereign debt amounts to two and a half times its GDP. The developed G20 countries borrow mostly in their own currency, which is why they can sustain higher levels of debt. More problematic is the situation in developing countries in and outside the G20, which need to borrow in foreign currency, because then they need to export in order to earn the revenues necessary to service the debt.

The 2016 Trade and Development Report of the UN Conference on Trade and Development (UNCTAD) assesses the phases of crises as beginning with the United States in late 2007, then spreading to the European sovereign bond market in a second wave, and now moving to the developing countries in a third phase. Prompted by low interest rates, developing countries have amassed the highest level of public debt ever recorded, with total debt stocks presently standing at around $5.4 trillion, with $575 billion in annual interest payments.[2]Research by Jubilee Germany[3] shows that 108 developing countries are in a more or less critical debt situation today – this is 25 more than last year.

Two current global trends in particular contribute to the build-up of new debt crisis risks in a broad range of developing countries: the drop in world market commodity prices and the high volatility of capital markets. Many developing countries are suffering from declining revenues since the prices for commodities they export (e.g., oil and minerals) have declined, sometimes steeply. When a downturn in commodity prices hits, countries need to take on more and more debt, not only to keep their economies from contracting too sharply, but also to repay earlier debt, incurred during boom times and to substitute for lower revenues.[4] At the same time, lower export earnings and the contraction of the economy lead to a ballooning of existing debt levels.

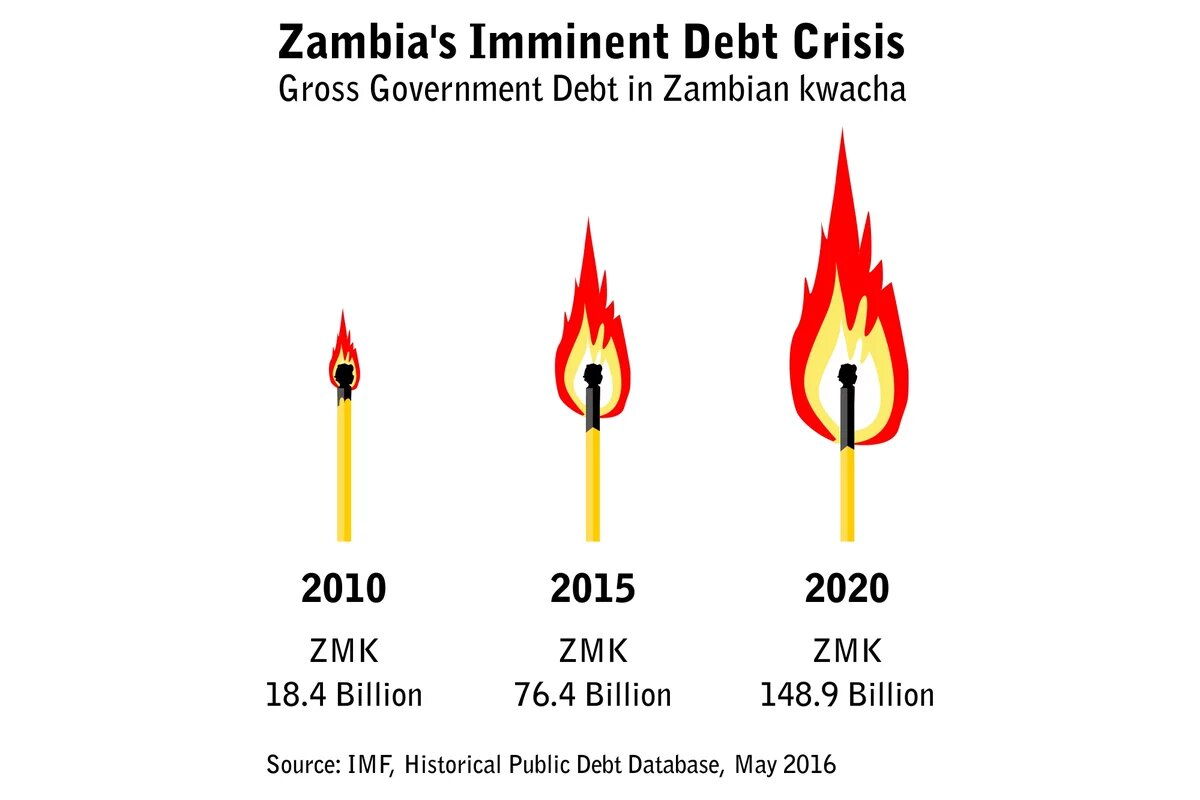

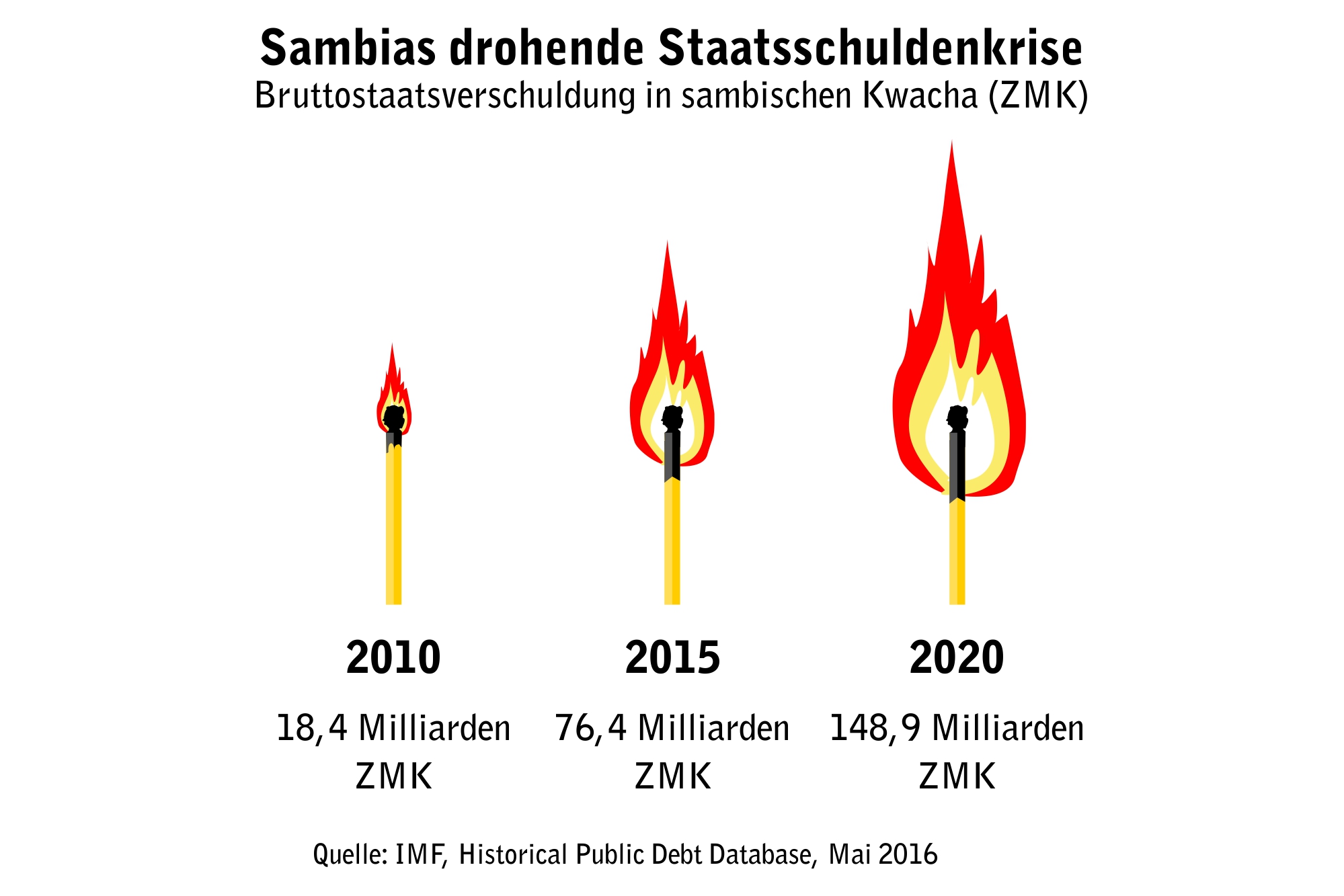

Take Zambia, for example: about 41 percent of its GDP is earned from exports of raw materials, three-quarters of which is copper. China consumed almost a quarter of the copper Zambia exported in 2014. In the first quarter of 2015, total exports declined by about 27 percent. Zambian mines are closing and the country’s currency has been the worst performing globally so far this year.[5] According to UNCTAD, Zambia can be considered at high risk of either a private or public sector-led debt crisis.[6]

2. What are the stated G20 goals and commitments in relation to this topic?

The G20 Communiqués from the past five summits indicate that the issue of public debt only made it onto the radar screen three years ago. A brief reference to the concern around high debt to GDP ratio first made its way into the Mexican G20 Leaders’ Communiqué in 2012 and subsequent communiqués. Overall, the four most recent G20 Communiqués have nothing significant to say on this topic. For instance:

- The Russian G20 Communiqué (2013): mentioned the update of the IMF’s Guidelines for Public Debt Management, ongoing work by the Organization for Economic Cooperation and Development (OECD) in this area, and the role of the IMF-World Bank Debt Sustainability Framework for Low-Income Countries in providing assistance to low-income countries in the areas of prudent debt management strategies and capacity-building.

- The Australian G20 Communiqué (2014) welcomed the work of the Financial Stability Board (FSB) on sovereign debt management and restructuring; in addition, it called on the inclusion of pari passu clauses in international sovereign bonds and encouraged the international community and private sector to actively promote their use. Pari passu clauses aim to enable creditors to be treated equally without preference (see Section 3 below.)

- The Turkish G20 Communiqué (2015) welcomed the progress achieved on the implementation of strengthened collective action clauses, which allow a significant majority of bondholders to force a debt restructuring that binds all bondholders, including the opposing minority, such as a vulture fund (see Section 3 below). It also welcomed pari passu clauses in international sovereign bond contracts, and took note of the Paris Club, which is an informal body of mainly Western bilateral creditors hosted by the French Ministry of Finance that deals with the restructuring of bilateral loans when needed. Many important G20 creditor nations, in particular China, are not members of the Paris Club.

- The most recent Chinese G20 Communiqué (2016) which built on the Turkish one, stated: “We underline the importance of promoting sound and sustainable financing practices and will continue to improve debt restructuring processes. We support the continued effort to incorporate the enhanced contractual clauses into sovereign bonds. We support. . . the ongoing work of the Paris Club, as the principal international forum for restructuring official bilateral debt, towards the broader inclusion of emerging creditors.”[7]

While the Chinese Communiqué implies that the door may have opened slightly for a future debate on the issue, these communiqués reveal no proactive reform agenda on the topic. Instead the G20 is merely welcoming work done by the IMF and to a lesser extent by the World Bank; furthermore, none of the communiqués mentions the work of the UN system, such as the UN General Assembly’s attempts to create a legal framework for sovereign debt restructuring, the work of the UN Conference on Trade and Development (UNCTAD) to establish the Principles on Promoting Responsible Sovereign Lending and Borrowing, or the UN Human Rights Councils’ work to establish the Guiding Principles on Foreign Debt and Human Rights.

3. What is the progress so far and the challenges in relation to this topic?

Ideally, loans would be made for productive projects or enterprises that would generate the kind of return necessary for repayment with interest. But, there is a long history of countries and citizens seeking to repudiate “illegitimate” sovereign debts that were taken on by dictators or pocketed in corrupt ways. And, years ago, the pressure to lend (petrodollars) was so strong that a whole generation of loans was thrust upon developing countries with cheap promises of prosperity. Then, to service these loans - often for “white elephant” projects – creditors imposed requirements for budget cuts (often to health care, education, water and other services), privatization, and liberalization.

The IMF and the MDBs became infamous for these “Washington Consensus” policies[8]in their structural adjustment programs. Later, IMF officials professed to over-selling certain neoliberal policies. While some of these loans from official lenders (such as multilateral development banks (MDBs)) applied environmental and social safeguards, these were equally loathed by debtor countries. As noted above, these countries also needed to cope with the problem that much debt was acquired in foreign currencies and, as a result, they needed to export more and more to earn the “hard currency” required for debt service.

Today, the sovereign loan landscape is even more complex with different instruments and players; for instance, government bonds pushed out bank loans, and private investors have largely replaced official lenders, such as MDBs or governments. The Bretton Woods institutions (the World Bank and the IMF) now have a smaller share of the debt “pie”, since they are already overtaken by new public lenders, such as multilateral and bilateral institutions of BRICS countries (Brazil, Russia, India, China and South Africa) and the private sector. Among the new creditors are a variety of private investors and bondholders. This means that the number of creditors that needs to be involved in the resolution of a debt crisis has increased massively, and the process becomes ever more difficult to coordinate.[9]

Some creditors choose to holdout and sell their claims to “vulture funds”; these are a specialized form of hedge funds that buy junk bonds of crisis countries cheaply (at prices far below nominal level) on financial markets and then, eventually, refuse to participate constructively in a sovereign debt restructuring process and, instead, sue the debtor for full payment.[10]

In this context, collective action clauses and the expansion of the Paris Club, both of which were discussed at the latest G20 summit, are insufficient to ensure the resolution of future debt crises. The Paris Club has been notoriously ineffective in restoring the sustainability of a country's debt. Countries often had to negotiate several times, because concessions granted by the Paris Club turned out to be insufficient. Furthermore, the way the Club works effectively hampers meaningful co-ordination across the various types of creditors.

Collective action clauses are useful instruments for reaching a binding agreement, once a restructuring of bonded debt is required. They can also help to minimize the problem of holdout creditors and vulture funds. However, the assumption that collective actions clauses could substitute for a comprehensive sovereign insolvency framework is unjustified, given the limited reach of these clauses. They support the restructuring of just one lending instrument, which means they are unable to solve the coordination problem between various asset classes.

Recognizing that action is needed when a country becomes insolvent, many have argued that the international financial architecture is missing a key element, a comprehensive sovereign debt restructuring mechanism. The IMF[11], noted economists[12], and civil society[13] have circulated proposals for such a mechanism for years and continue to do so. Implicit in these proposals is the fact that, as a general rule, debtor countries share responsibility with lenders for their predicament. Multiple soft law instruments set standards on sovereign debt management and restructuring[14], but implementation is confused and fragmented. International institutions, such as UNCTAD, and civil society organizations, such as the European Network on Debt and Development (EURODAD), are promoting responsible borrowing and lending in order to prevent debt crises. When there is a failure to prevent debt crises and they must be resolved, we will benefit from a new set of rules, a new legal regime to address the situation of sovereign insolvency, and an institution building effort. The time is ripe to revitalize these discussions, and the UN is prepared to table another discussion on debt issues later this year. The G20 countries, Germany for example, must not throw obstacles in the path of this multilateral process.

4. What is the desired future direction of the G20 with respect to the topic?

The German G20 gives high priority to the issue of investment in Africa, particularly for infrastructure. Debt levels in Africa have risen considerably in the last several years, as many countries have been hit by shocks, such as declining demand and prices for their commodities. Added to this there is the risk of private debt turning into public debt through bailouts. It is crucial that fiscal commitments to large infrastructure projects not compromise other obligations of the state or tip more nations into a condition of debt distress.

In Africa and elsewhere, the G20 countries should consider the following actions as part of their exercise in leadership:

- Responsible Lending and Borrowing. Explore ways to ensure responsible lending by G20 governments, as well as by the sovereign wealth funds of G20 countries that are investors in sovereign debt, and private sector financial institutions. Responsible lending can protect not only debtor nations but also lenders: their loans would not be seen as “illegitimate” in the first place, which could lead to calls for debt cancellation. To this end, support the 2012 UNCTAD Principles on Promoting Responsible Sovereign Lending and Borrowing (applicable to all countries) and the 2011 EURODAD Responsible Finance Charter (aimed at lending to development countries with emphasis on development). These would help overcome the fragmented nature of other voluntary standards related to lenders’ accountability and public debt management.

- A needs- and rights-based approach to debt sustainability: To ensure compatibility with the Sustainable Development Goals, debt sustainability assessments should - first and foremost - assess whether a country's debt payments are preventing the financing of human and environmental needs. In addition, any revision of the IMF-World Bank Debt Sustainability Framework should fully reflect not only the weight of domestic and external debt, both public and private, but also the contingent liabilities taken on by governments to offset the risks of private investors in Public-Private Partnerships.

- Sovereign Debt Restructuring Mechanism. Reintroduce the latest thinking on options for a Sovereign Debt Restructuring Mechanism. The Debt20 campaign backed by a global coalition of civil society organizations expects the 2017 G20 process to build on the discussions of the Chinese G20. The G20 should acknowledge the threat of the new sovereign debt crises in the Global South and support the creation of a comprehensive sovereign debt workout mechanism based on rule of law.

- National vulture funds legislation: G20 countries should lead by example and enact laws against vulture funds, as Belgium and the UK already did.

As the German government shapes its proposal for a “Compact with Africa” in consultation with African and other G20 governments, the Civil 20 (taking the lead from African civil society networks) is providing input to decision-makers as well. The above recommendations are important in this context and, in particular, civil society will focus on helping to ensure responsible lending and borrowing to ensure that future generations are not unfairly burdened by new debt.

(Photo by CafeCredit under CC 2.0)

Annotations:

[1] Ostry, Jonathan D.; Loungani, Prakash; Furceri, Davide: Neoliberalism Oversold?, in: Finance & Development, June 2016, Vol. 53, No. 2, S. 38–41.

[2] International Debt Statistic, World Bank (2016)

[3] erlassjahr.de (2016): Global Sovereign Indebtedness Monitor. According to IMF’s assessment of debt distress risks, as of 1st September 2016, 17 of 70 examined low income countries have a high risk of debt distress, and 35 have a moderate risk of debt distress (which means that if an external shock hits in the future, debt indicators get critical).

[4] External Debt Sustainability and Development, UNCTAD (2015)

[5] Friedman, George: The Export Crisis. The 10 Worst Hit Countries and the 5 Most at Risk. Published by Geopolitical Futures, 21.1.2016.

[6] UNCTAD (2016): Africa – Report 2016. Debt Dynamics and Development Finance in Africa. Available also in a original version.

[7] G20 Leaders’ Communiqué Hangzhou Summit, par.17.

[8] see Ostry et al.

[9] Ellmers, Bodo: The evolving nature of developing country debt and solutions for change, Eurodad (2016).

[10] See Caliari, Aldo: Nicht noch ein Spielball der “Geierfonds“, (2015); also see the UN Human Rights Council process of investigation into the negative human rights impacts of vulture fund activities.

[11] For example, the IMF/World Bank’s Guidelines for Public Debt Management (revised in 2014); the FSB Guiding Principles for Managing Sovereign Risk and High Levels of Public Debt ("Stockholm Principles") (2010); and the OECD Working Papers on Sovereign Borrowing and Public Debt Management.

[12] “A New Approach to Sovereign Debt Restructuring”, IMF (2002).

[13] For example, Guzman, Martin; Ocampo, José Antonio; Stiglitz, Joseph E.: Too Little, Too Late: The Quest to Resolve Sovereign Debt Crises. Columbia University Press, 2016.

[14] Kaiser, Jürgen, erlassjahr: Resolving Sovereign Debt Crises Towards a Fair and Transparent International Insolvency Framework. Friedrich Ebert Foundation (2013).

{kind=link}

{kind=link}

{kind=link}

{kind=link}