Analysis

China produces more than 30 percent of global emissions. In this article, Adam Tooze explains why the People's Republic's next five-year plan will have a decisive impact on the global climate - and why this is reason for cautious optimism.

Summary

China plays a crucial role in the global climate as it is responsible for over 30 percent of global emissions. The next five-year plan and new national emission reduction targets could set the country on a path to decarbonization. Measures such as the massive expansion of renewable energies, the reduced permission of new coal-fired power plants and changes in the steel and cement industries could reduce China's emissions by 30 percent by 2030 and thus give new impetus to climate protection worldwide.

China is the most important driver of worldwide emissions. Rich western countries have accumulated more total emissions. Other developing countries have emissions that are rising more rapidly than China’s. But China’s scale makes it different. China alone now accounts for more than 30 percent of global emissions, twice the share of the United States. In the ten years since the Paris agreement of 2015, China alone has been responsible for 90 percent of the growth in global CO2 emissions.

Some of China’s emissions are attributable to exports delivered to world markets. But as a huge importer of raw materials and semi-finished products China also outsources emissions. And it is above all China’s domestic energy use that accounts for this huge surge in emissions.

China’s economic development in the last half century is blandly described as the great acceleration 2.0. It is, in fact, the greatest development surge in human history driven above all by an unprecedented and spectacular surge in urbanization.

Comparisons can be helpful in scaling this. But they are technically tricky and GDP numbers are deceptive. According to the GDP figures China is either still catching up with the United States or marginally ahead. As to the physical scale of production this is utterly misleading. As a physical productive apparatus China completely dwarfs the United States (and any other comparator). China’s total electricity generation is twice that of the United States. China’s steel production is ten times that of the USA. China’s cement production is more than twenty times that of the USA.

These are elementary facts, but they cannot be restated too often. In the environmental history of our species China is not a continuation of the “Western story”. It is its own chapter, or even its own volume. It is China’s story, more than any other, that defines our current horizon of expectation and the scope of our current possibilities.

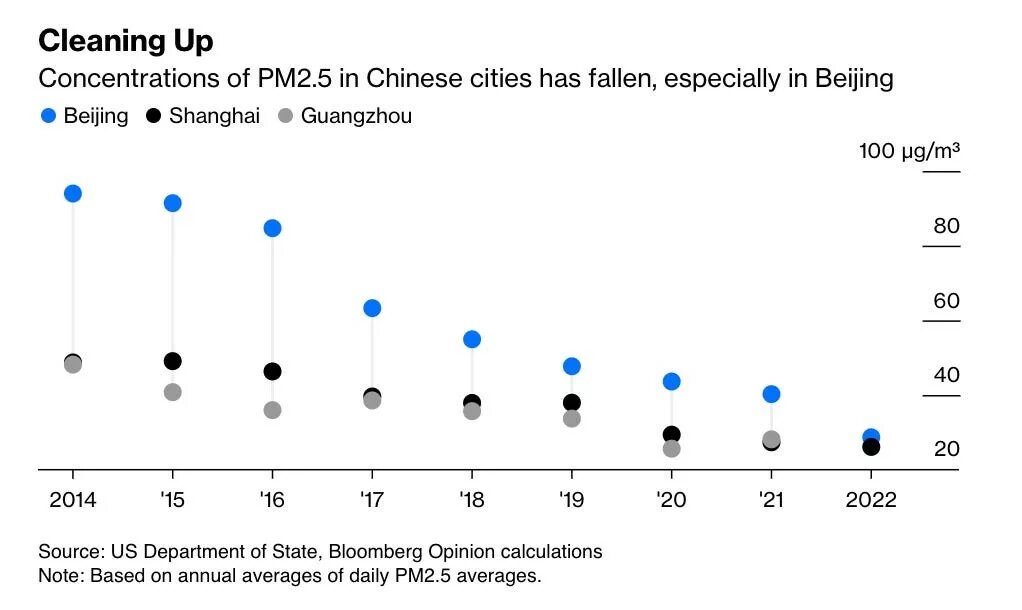

As the scale and implications of this surge in environmental impact dawned on Beijing, China’s government was instrumental in forming the new climate regime solemnified at Paris in 2015. Without China’s promise made in 2014 to achieve a peak in emissions around 2030, it is hard to see how the Paris climate accords would have come about. The decision was taken for both global and local reasons. There is much speculation both inside and outside China about the propaganda value of clean air campaigns. There can be no doubt that since the catastrophic mega-smogs of the early 2010s, the air quality in China’s largest cities has been transformed. Air pollution standards have been drastically tightened and power generation has been shifted to the Western provinces where both fossil and renewable power generation is increasingly concentrated.

This is a vital moment both for China’s domestic environment and for global climate policy.

In 2020 Xi Jinping concretized China’s climate commitments with the goal of achieving neutrality by 2060. That in turn helped to trigger India and others into announcing similar targets. Now, as the Paris climate targeting process grinds on, by February 2025 China must announce its Nationally Determined Contribution to decarbonization. At the same time Beijing is also preparing to formulate the 15th Five-Year Plan, which will run 2026-2030. As I argued in another Chartbook earlier this year, this is a vital moment both for China’s domestic environment and for global climate policy.

How exactly they impact global balances is a matter of forecasting and accounting. Earlier in the year, the estimates by CREA of possible transition paths for China, left me very pessimistic about the feasibility of a path that holds warming to 1.5 degrees. These numbers have subsequently been critiqued and revised by Chinese climate expert and reporter Jiang Yifan in a piece in the Chinese edition of the FT. In a revision that is conceded by Lauri Myllyvirta, Jiang Yifan has shown that if China adopts a crash decarbonization program its share of the remaining emissions on 1.5 degree path would be 44 percent, which is huge but not entirely inconceivable. If we accept a 2 degree path as more likely, then depending on the pace of Chinese decarbonization, China’s share of the remaining carbon budget lies between 12 percent, were Beijing to force through crash decarbonization, and 23 percent on a more delayed path. As Jiang Yifan goes on to argue:

„Choosing (an ambitious 1.5 degree path) will show China's strong commitment to the Paris Agreement goals and exhibit its climate leadership as a big nation. Furthermore, if both China and the world aim for 1.5°C, then when achieving carbon neutrality, China will account for about 15% of the more than 2.8 trillion tons of cumulative CO2 emissions since the Industrial Revolution. If the world settles for 2°C while China still aims for 1.5°C, then China will account for about 12% of the more than 3.5 trillion tons. The 12%-15% range is higher than the UN's World Population Prospects 2024 projection of China's share in the world population in the year 2060, which is about 11%. Therefore, domestically, this could also be seen as a relatively fair historical share of emissions for China.“

Clearly, whichever path Beijing chooses, it will have a huge impact on the entire global balance.

Given the scale and relative dynamism of the Chinese economy, the path of Chinese emissions is worth tracking on a quarterly basis. If making the climate crisis into an exciting news story is a problem, China’s emissions are part of the solution. At least four times a year we should be checking in to get a new read on our collective futures and thanks to experts like Lauri Myllyvirta and the team at CREA, we can do this in real time.

Of course, we should be doing the same for the West as well, just don’t expect the action to be as exciting.

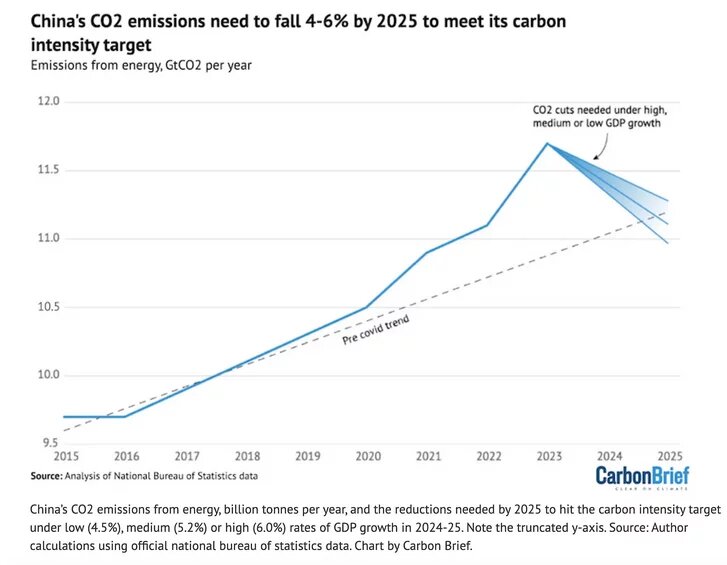

Because the Chinese economy is so industry-heavy, whenever growth picks up, it has dramatic implications for energy use and CO2 emissions. Though China’s growth is overall slowing down, the aftermath of COVID saw one last burst of very rapid growth in emissions. Combined with a drought-induced slump in hydropower generation, this has put China severely off-course to meet its existing carbon-intensity targets.

Emissions in China may be peaking right now

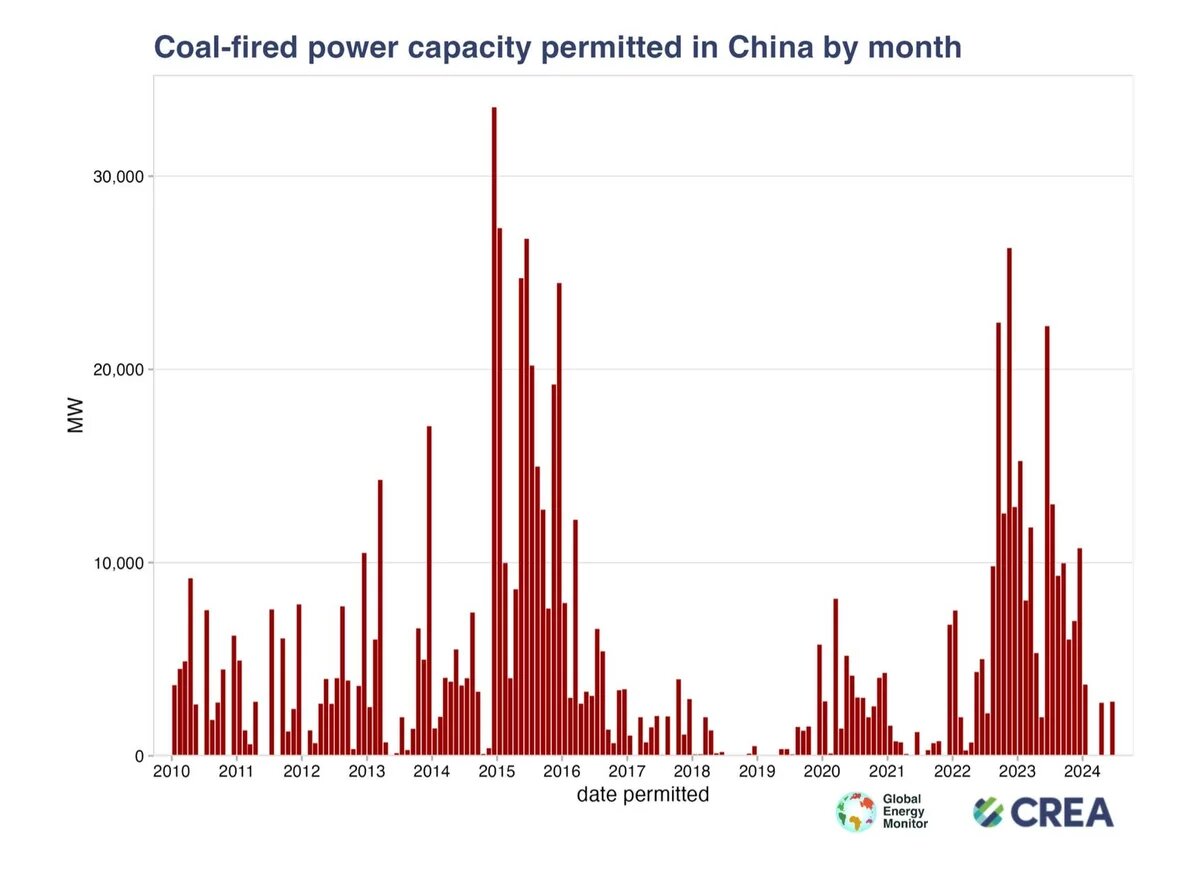

The post-COVID shock will have long-lasting implications because in 2022-2023, it went hand in hand with a surge in coal-fired power station permitting. In those two years alone China permitted over 200 GW of new coal fire power stations. That is the equivalent of the entire installed coal power capacity in North America, in new permits, in only two years. Over that period China accounted for 70 percent of all new coal fired capacity permitted worldwide. (This, paranthetically, is what I mean by saying that China drives the global dynamic!)

But in 2024 China turned on a dime. In the first half of 2024 it slashed coal-power permitting by 83 percent, to only 9 GW.

What experts are now debating is whether we may be witnessing the moment at which emissions in China peak. If so, it would mark a true turning point in global climate history.

The optimistic case hinges on dramatic developments in the Chinese green energy space in the last few years.

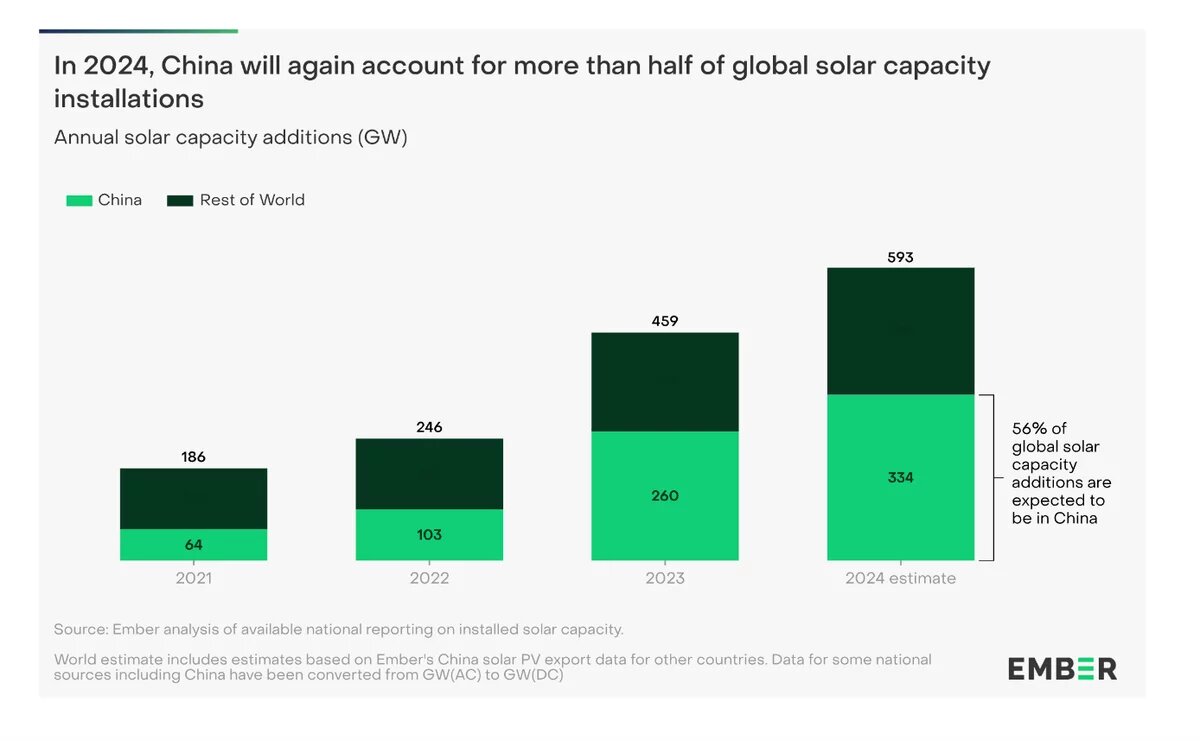

In 2023 China added 293 GW of new wind and solar power capacity, just shy of the total solar and wind capacity installed in the USA, in new installation in a single 12 month period. Estimates suggest that even more renewable capacity will be installed in 2024. For two years in a row, China will install more green energy capacity than the rest of the world put together.

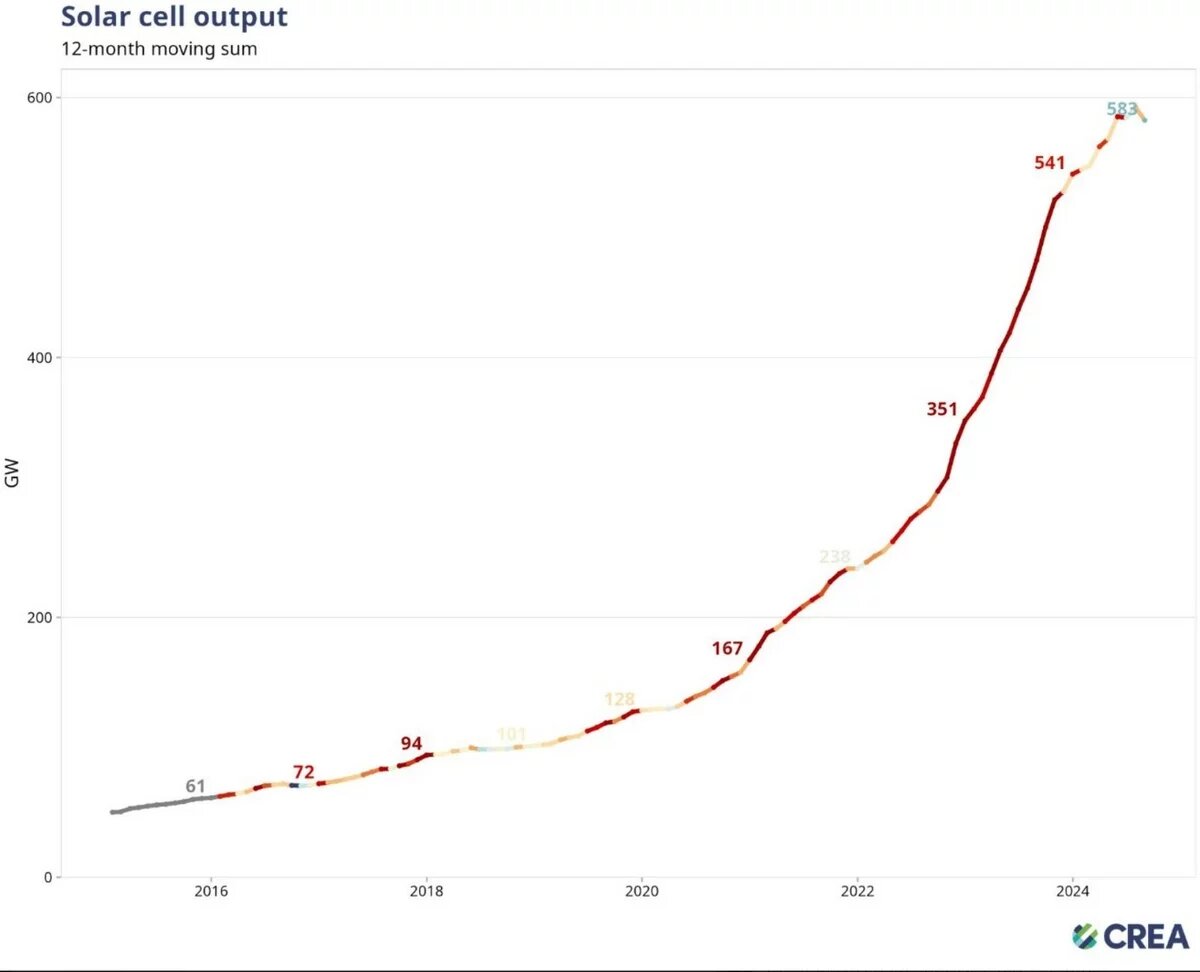

The huge surge in Chinese solar cell manufacturing is arguably the most optimistic piece of news in the world economy. It is tough for the manufacturers themselves. Competition is fierce. But China’s immense surge in capacity puts affordable solar electricity within reach of even the poorest societies. The 13 GW surge in exports of cheap PV to Pakistan that are transforming that country’s power grid, are a rounding error in the Chinese production numbers.

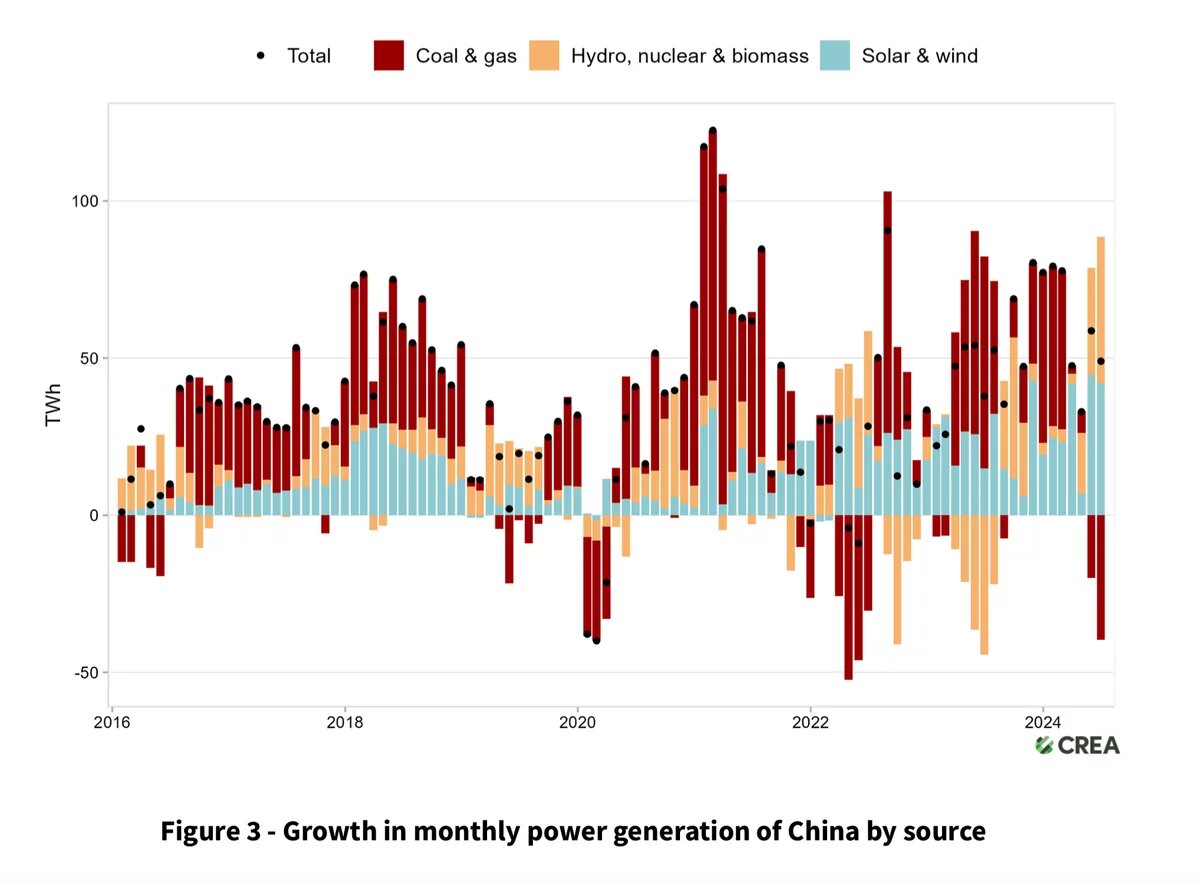

In China itself, for the first time, new clean energy capacity is more than covering the incremental increase in energy demand.

In China itself, for the first time, new clean energy capacity is more than covering the incremental increase in energy demand. In due course this will eat into China’s giant mountain of coal-fired capacity.

According to one set of estimates, the 400 GW of new solar and wind power that have been added since 2023 have driven down China’s coal power generation by 7 percent.

This trend is reinforced by the shift from heavy-industrial growth to what Beijing calls “new quality productive forces”, of which microelectronics and “new energy” are leading sectors. In the green energy space this is a trend incentivized by government policy but led by the private sector. According to one set of estimates from the CREA team reviewed in an earlier Chartbook, in 2023, the clean energy sector contributed 40 percent to China’s GDP growth, making green growth the dominant driver for the first time in a major economy.

In recent months the shift to new quality productive forces has been raised in the CCP hierarchy, to the status of Deng’s historic reform program of the 1980s. From the point of view of the global environment this is no exaggeration. The new industries - like microelectronics and green energy - are by no means carbon neutral. According to the think tank Carbon Brief:

“The clean energy manufacturing boom also has a role in driving emissions, due to energy-intensive processes involved in the production of solar PV and batteries, in particular. Approximately one percentage-point of CO2 emission growth can be attributed to these sectors, based on output data and emission intensities estimated for solar PV, electric vehicles and batteries. This means that, without the clean technology manufacturing boom, China’s CO2 emissions would have grown by around 4.2 percent, instead of the 5.2 percent estimated in our analysis. Nevertheless, the increase in manufacturing will result in a significant reduction in emissions in net terms, once the products are in use. About half of this reduction will be realised outside of China, as the products are exported.”

But though green growth in China is not carbon free it is less carbon-intensive than the old heavy industrial productive forces that it is replacing i.e. steel and cement. Between 2020 and 2023, cement output and emissions fell by 15 percent and the trend is further downwards.

Chinese steel production is still immensely carbon-intensive because rather than recycling used steel in electric arc furnaces, China continues to produce iron in classic blast furnaces which are hugely coal intensive. In future, as Chinese heavy industrial growth slows and old steel can be recycled, there are vast gains to be made in efficiency and decarbonization. The China Iron and Steel Industry Association believes that by 2035 as much as 30 percent of Chinese steel production could come from electric arc furnaces. If this were combined with a modest reduction in overall output this should enable major cuts to emissions.

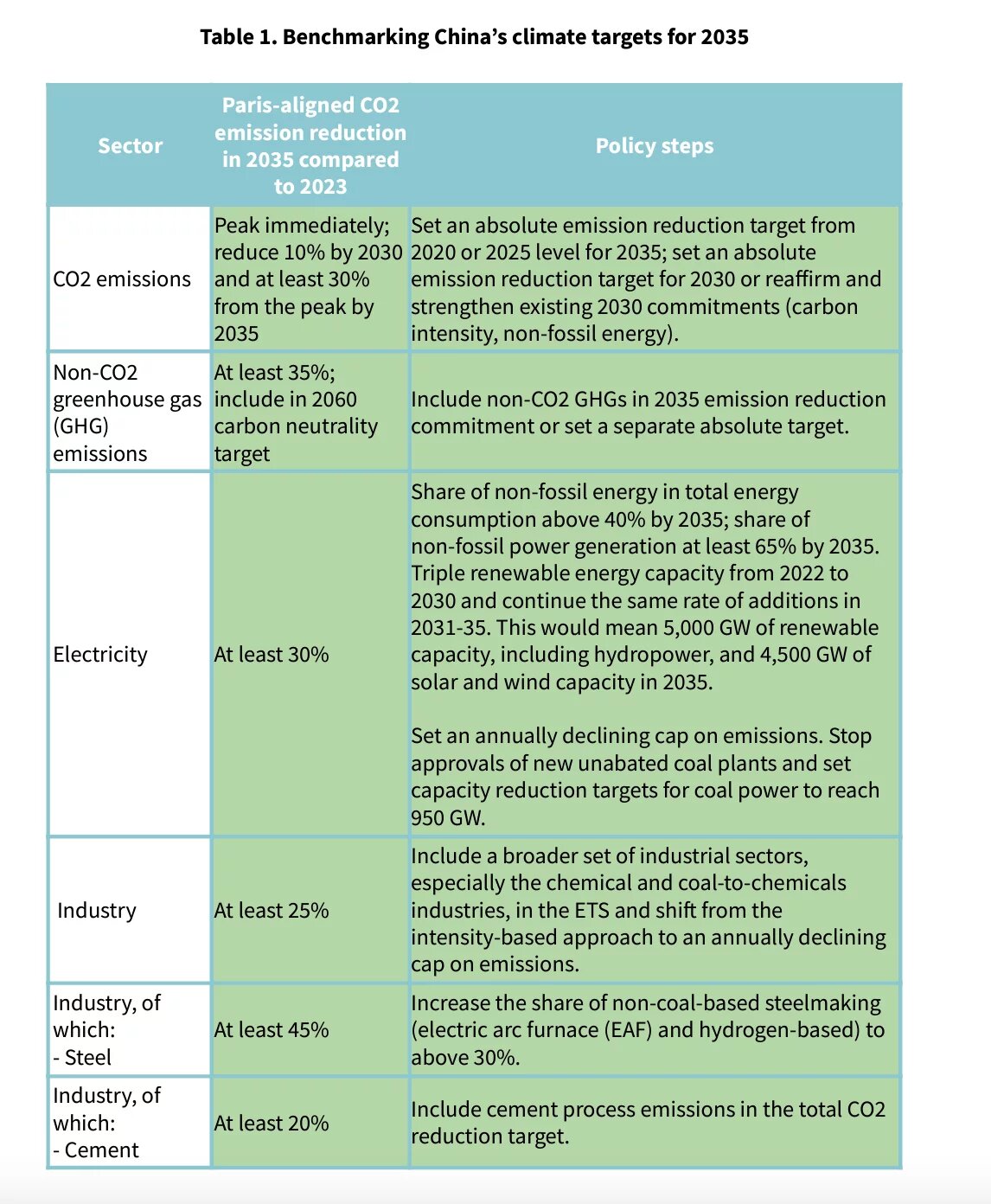

It is these developments that put more ambitious goals for China in 2025 within reach. In July 2024, the 20th Central Committee of the CCP released a communique from its Third Plenary Session, which, for the first time, mentioned "carbon reduction". China’s 2024-2025 energy saving and emission reduction plan has again underscored the priority of controlling emissions. And to this end the permitting of new coal-based steelmaking has been suspended. So, if one had the ear of Beijing, what should China’s Nationally Determined Contributions to be announced by February 2025, look like? Once again, a helpful guide has been provided by the CREA think-tank.

To stay roughly in line with a Paris-confirming trajectory, China needs to achieve 30 percent reduction in emissions by 2035. Not a relative reduction in carbon intensity, or an uncoupling of growth and emissions, but an actual reduction in emissions.

If China embraces its current trends and leans into the radical overhaul of its energy system - in itself a daring proposition, but essential if ambitious goals are to be achieved - it could by 2030 install 3,500 gigawatts. By 2035, 5000 GW are within reach. By 2035 those clean energy sources could supply 65 percent of power generation. That would allow a 30 percent reduction in emissions from the electricity sector, which would be a huge step towards meeting net zero objectives. Cleaner electricity then gives a powerful rationale to the rapid roll out of Electric Vehicles that is already happening in China’s most affluent cities. Nationwide the adoption of EVs in China is so rapid that it is ahead of the most optimistic 1.5 degree pathways. It lags significantly in poorer parts of the country with less good infrastructure. China also needs to shift a far larger share of its freight transport off the road onto rail. And it needs to push decarbonization into industry, notably steel and cement.

China has recently announced that it is extending its emergent emission trading scheme (ETS) to include steel, cement, and aluminium sectors. As we know from experience in the EU, contrary to prevailing wisdom in the US, ETS systems can work. But they work only if they are given teeth in the formeof a steadily tightening emissions caps and comprehensive reach. In the Chinese case, the system must be extended to the chemicals sector. Carbon pricing will be painful to apply to a sector like cement that is expecting to see its demand fall by a further 10 percent by 2030. But combined with rationalization and the concentration of production on the most modern and cleanest plants, it should enable reductions in emissions from cement that are close to 30 percent relative to 2020. In China, as elsewhere, decarbonizing the building sector is a huge problem with vast needs for retrofitting and simply gigantic quantities of heat pumps. But China can make a start simply by eliminating, as far as possible, the domestic use of coal for home heating.

All told, the dashboard for a high-ambition NDC with targets for 2035 according to the CREA team, would look like this:

As is normal for this kind of exercise, the CREA team emphasize the positive. And China has demonstrated the capacity for huge and innovative growth. But decarbonization is also about tough trade offs. The fossil-fuel sectors have to be wound down. In the West there is much talk about “just energy transitions” in which workers in fossil fuel sectors are compensated. Nowhere is that kind of program more urgently needed than in China. Energy expansion was relatively easy when the Chinese economy was growing fast. It will be tougher as growth slows.

It would not be true, however, to suggest that Beijing has no experience with shutting down or rationalizing excess capacity. Since China’s 13th Five-year Plan (2016-2020) set rationalization and modernization of the coal industry as a key priority, more than half of Chinese coal mines – the least productive and unsafe ones – have been closed. This has resulted in a halving of coal employment from a peak close to 5.5 million in the early 2010s. It has also yielded a 80% reduction in coal mining fatalities. And all without any significant reduction in coal production capacity. It did however leave the system vulnerable to shocks, as was apparent in 2021-2022, when coal supply became an acute problem. The challenge for future decades is to continue the orderly wind-down with a concentrated effort to find alternative paths for development for the economies of Inner Mongolia, Shanxi and Shaanxi. New green energy investment will be a key part of their regional future. We will come back to the future of the Chinese coal industry in a future post.

These are the familiar tough challenges of decarbonization. China faces them on a far larger scale than anywhere else. But it also faces them with an economy that is used to 40 percent or more of GDP going to new investment and an absolutely unrivaled capacity for industrial production and innovation. As the new energy sector is demonstrating, this gives it the capacity to act on the necessary scale and at pace.

For all of these reasons, the decision to be made by Beijing in the coming months is momentous. China’s emissions targets are vital to the achievement of global climate goals. They provide an encouraging signal to other actors that concerted action is worthwhile. In recent COP meetings China has come under vigorous pressure by other countries to act concertedly on its emission. The expansion of China’s green energy capacity is world historic in its implications. But it is not enough even to offset China’s own dirty growth in recent years. China will fall short of its 2025 targets. So ambitious and credible targets for 2030 are essential. By ensuring that there is large domestic demand for green energy goods China can also help to defuse trade tensions around Chinese exports of batteries, PV and electric vehicles.

The inside politics of China’s energy and emissions planning is technical and, for many, it is off the beaten track. It gets drowned out by the violence in the Middle East and Ukraine, and by the din of the US election. But once you realize the stakes in this decision, the sense of weight and drama is inescapable. In the next few months Beijing is planning not just China’s, but all our futures.

This article first appeared in the 324th edition of Adam Tooze's newsletter "Chartbook".